New legislation about credit freezes recently warmed the hearts and pocketbooks of millions of U.S. consumers. The new law, put into effect September 21st of this year, enables American consumers to place a credit freeze at the big three credit bureau’s: Equifax, TransUnion, and Experian – at zero cost. Although that option has always been there, for the first time that freeze is free for all. Before this legislation, it could cost consumers $10+ to do this – in addition having to pay to un-freeze it. This new law, officially known as “SB2155” allows all consumers to freeze and un-freeze their credit for free. It’s a victory for all U.S. consumers, whether they believe they need the service or not.

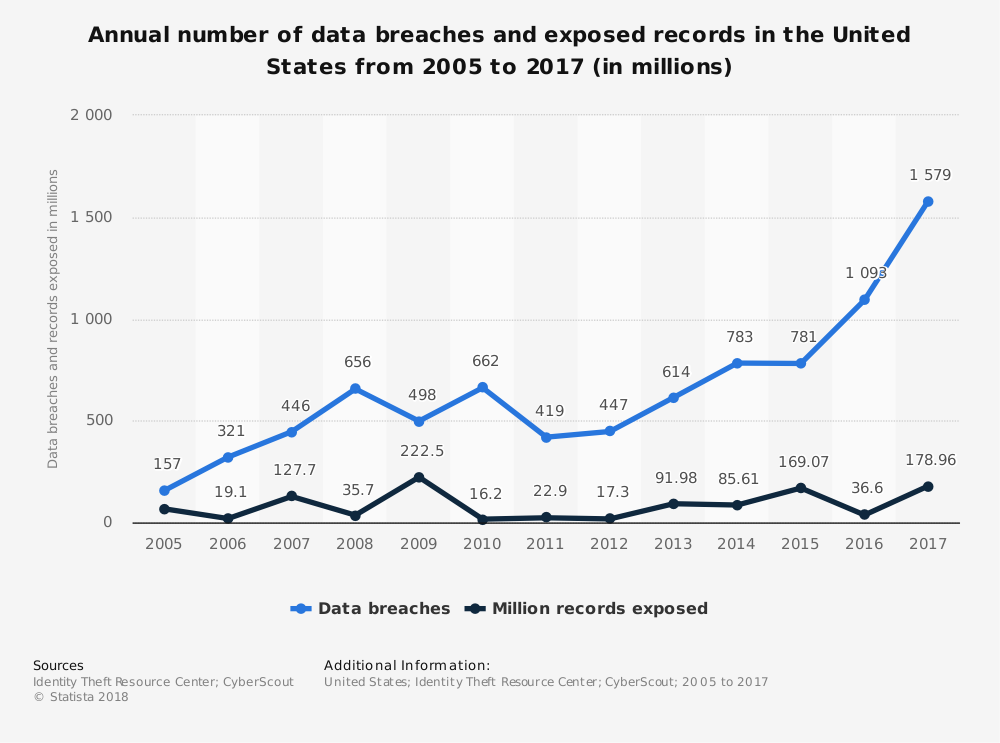

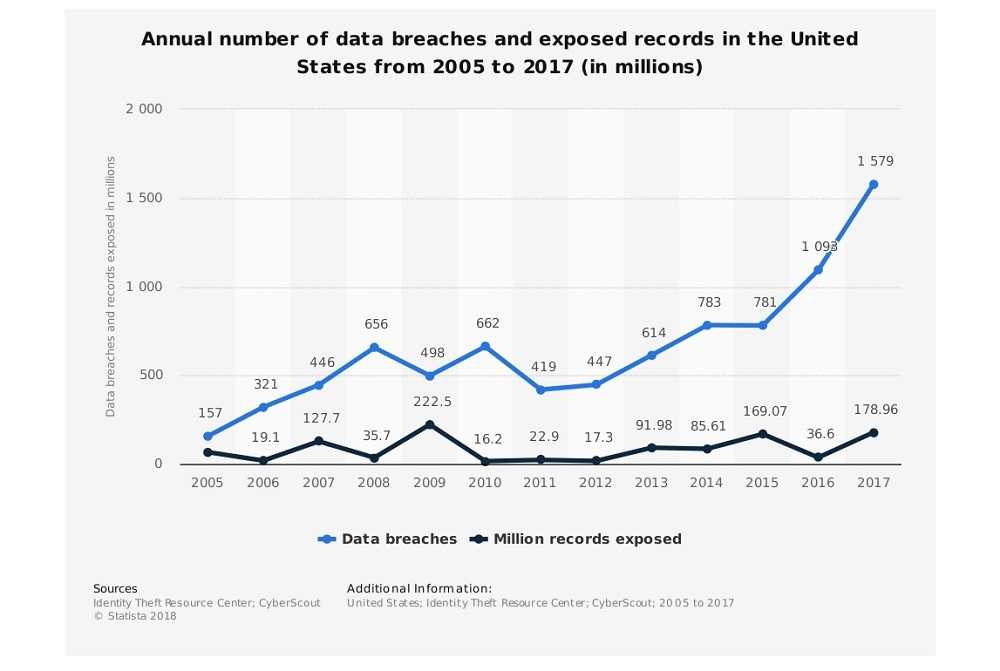

However, if you weren’t considering a credit freeze before, the way data breaches are increasing in size and scope, it may not be long before a freeze is needed. In 2017, both the number of data breaches and the number of exposed records in this country reached the highest ever. In 2017, Statista reports 179 million records were exposed in the U.S., with the total number of breaches reaching 1,579 for that year.

The legislation is due in large part as a response to the sharp increase in data breaches in this country and the world over. In 2017, the Equifax breach leaked financial data and other PII (Personally Identifiable Information) including Social Security numbers and driver license information of 148 million Americans. And who could forget the mother of all data breaches – Yahoo in 2013, exposing the PII of 3 billion users – and still counting. In June of this year, the number one data breach (so far) of 2018 came from a company called Exactis that allowed a data breach releasing 340 million records of U.S. citizens. The new legislation is surely a win for consumers, but it’s also an acknowledgment by the government of the increasing number of data breaches and the sensitivity of the PII they expose.

WHAT DOES A CREDIT FREEZE DO?

A credit freeze completely stops the ability to open financial accounts in your name and for the length of time of your choosing. It prevents anyone from getting access to your credit report; including you. Unlike credit monitoring or fraud alert services, which alert you only after suspicious activity occurs, a freeze stops any and all credit access and activity. Should you need to open access to your credit for things like buying a car or applying for a mortgage or loan, a temporary thaw can be placed so your credit history can be briefly accessed. Once done, the freeze can be renewed.

A credit freeze completely stops the ability to open financial accounts in your name and for the length of time of your choosing. It prevents anyone from getting access to your credit report; including you. Unlike credit monitoring or fraud alert services, which alert you only after suspicious activity occurs, a freeze stops any and all credit access and activity. Should you need to open access to your credit for things like buying a car or applying for a mortgage or loan, a temporary thaw can be placed so your credit history can be briefly accessed. Once done, the freeze can be renewed.

Remember, it’s always a good idea to check your credit report every few months. Each of the three credit bureaus offers one free credit report per year. Some financial institutions also offer their customers a free credit report. Just make sure when taking advantage of free offers, you read the fine print. If you are required to enter a payment card number to have access, you are possibly at the wrong website. The site annualcreditreport.com is the only one approved for these free reports by the U.S. government. Consider staggering when you order them to keep better tabs on changes.

HOW DO I GET A CREDIT FREEZE?

- Equifax: Go directly to their website or call their automated phone service line at 1-800-685-1111.

- Experian: Go directly to their website or call 1-888-EXPERIAN (1-888-397-3742).

- TransUnion: Go directly to their website. They also have a “myTransUnion” mobile app found at the Google Play Store and Apple’s App Store.

Remember when entering PII into any website, make sure it’s the legitimate one and that it has the “https:” at the beginning of the address. That is the indicator that the information you enter is secured.

SUBSCRIBE TO WEEKLY NEWSLETTER

SUBSCRIBE TO WEEKLY NEWSLETTER